BHP

BHP Snapshot

| FY1 | FY2 | |

|---|---|---|

| Price to Earnings: | 12.1 | 11.2 |

| Dividend Yield (%): | 5.6 | 5.1 |

| Price to Book: | 3.5 | 3.1 |

| Return on Equity (%): | 28.9 | 27.6 |

| EV/EBITDA: | 6.1 | 5.7 |

A Nickel Thorn on the Side

Shares in the Big Australian, BHP (ASX.BHP), announced lower full-year production guidance in the Queensland coal operations after a “tough six months” for the 1H24 period. Another headache for management is the substantial dip in nickel prices – falling nearly 50% – following an increase in nickel exports from Indonesia, fuelled by Chinese investment. The weakness in nickel prices has pushed management to evaluate options at the Nickel West operations in WA; we expect an update next month.

Before moving on to the quarterly update, a quick look at the technicals and after encountering resistance at $50, BHP has corrected back toward the primary uptrend that has been in place since 2020. Whilst the stock could go lower, the primary uptrend should hold. Below $45, BHP is in buying territory. Iron ore prices should soon find a floor.

2Q24 Trading Update

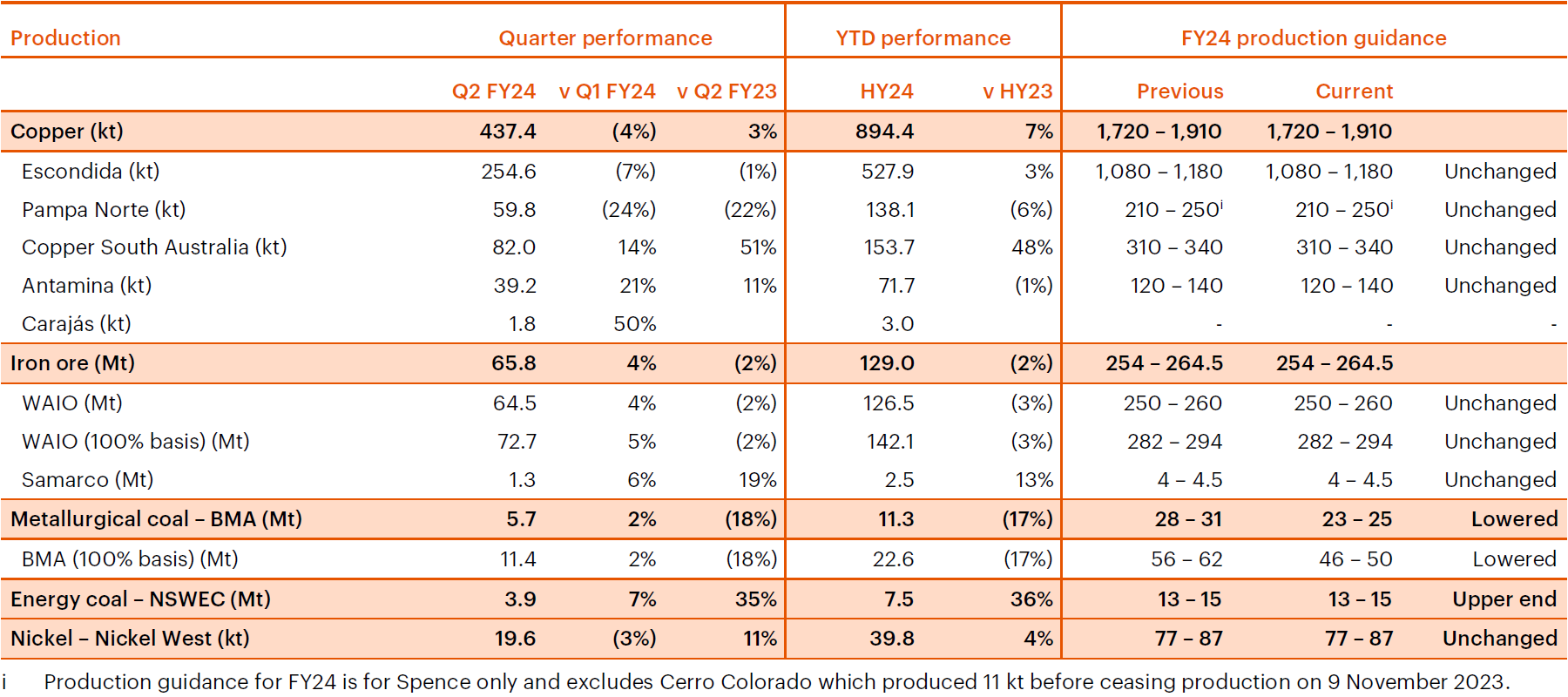

Starting from the top, BHP experienced a strong first half in copper, iron ore, and energy coal but faced challenges in metallurgical coal.

In terms of operational performance, the highlights are: [subscribe_to_unlock_form]WA Iron Ore production increased by 5% quarter-on-quarter, and first-half copper production rose by 7%. NSW Energy Coal had its best first half in five years. BMA (metallurgical coal) had a tough six months due to planned maintenance and low starting inventories. Nickel West is evaluating options to mitigate the impacts of a sharp fall in nickel prices.

Source: BHP 2Q24 Filing

Source: BHP 2Q24 Filing

On specific segment performance, starting with Copper. Total copper production increased by 7% to 894 kt. Escondida, Pampa Norte, and Copper South Australia contributed to the growth. Spence recorded a half-year production record, but Cerro Colorado entered temporary care and maintenance.

Next, Iron Ore. Total iron ore production decreased by 2% to 129 Mt. Lower production in WAIO due to tie-in activity for the Rail Technology Programme and ongoing ramp-up in the Central Pilbara hub. Samarco production increased by 13% due to higher concentrator throughput.

While for Coal, BMA production increased by 17% to 11.3 Mt but faced challenges, including a fatal incident at Saraji mine. NSW Energy Coal production increased by 36% to 7.5 Mt. Full-year production guidance for BMA lowered to between 23 and 25 Mt. NSW Energy Coal production guidance for FY24 expected to be at the upper end of the range of between 13 and 15 Mt.

Moving on, BHP also highlighted challenges in Nickel operations. While iron ore and copper prices have been impacting BHP’s revenue, nickel, a smaller percentage of its revenue, is causing additional concerns. There was the fact that Nickel fell 50% year-on-year. The nickel industry is experiencing structural changes, with increased supply from Indonesia contributing to a decline in nickel prices.

There is a call for a more transparent pricing mechanism that distinguishes between clean and dirty nickel, particularly as the environmental impact becomes a significant consideration, especially in the electric vehicle (EV) market.

For the quarter, BHP notes quarterly nickel production increased by 4% to 40,000 tonnes, but the average realized price dropped by 24% to US$18,602/tonne. BHP acknowledged that the nickel industry is undergoing structural changes and is facing a cyclical low in realized pricing.

That and BHP is actively optimizing operations and evaluating options to counter the challenges posed by the sharp fall in nickel prices. Management is conducting a carrying value assessment of its nickel assets under existing market conditions, with further details expected in the financial results release next month on February 20.

Nickel West, a key part of BHP’s nickel operations, is actively exploring options to mitigate the impact of the significant decline in nickel prices. BHP Nickel West Asset president Jessica Farrell highlighted the tough operating environment, with rising costs and falling Nickel prices. Nickel West is described as a complex business involving underground mining, third-party supply, on-site smelting, downstream refining, and a multi-stage supply chain.

Meanwhile, BHP has decided to pause part of its Kambalda processing operations in Western Australia, following Wyloo’s decision to place several nickel mines under care and maintenance.

Going forward, management has kept production guidance for FY24 unchanged for most assets, except BMA, which lowered its production guidance. Unit cost guidance increased for BMA to between US$110/t and US$116/t due to lowered production guidance.

Summary

BHP’s operational review highlights a mix of strong performance and challenges across its key segments. While copper, iron ore, and energy coal showed positive results, metallurgical coal (BMA) faced difficulties. The fatal incident at Saraji mine is a tragic event, and BHP is committed to learning from it.

The growth agenda is progressing, with the ongoing construction of the Jansen mine and the sanction of Jansen Stage 2. Exploration drilling beneath Olympic Dam has identified promising copper mineralisation.

Financially, production guidance remains stable for most assets, except BMA, where production guidance was lowered. Unit cost guidance for BMA increased due to the lowered production outlook.

In the meantime, while we wait out further improvements to the commodity prices, we maintain our HOLD rating on BHP.

Disclosure: Interests associated with Fat Prophets hold shares in BHP.[/subscribe_to_unlock_form]

Fat Prophets has made every effort to ensure the reliability of the views and recommendations expressed in the reports published on its websites. Fat Prophets research is based upon information known to us or which was obtained from sources which we believed to be reliable and accurate at time of publication. However, like the markets, we are not perfect. This report is prepared for general information only, and as such, the specific needs, investment objectives or financial situation of any particular user have not been taken into consideration. Individuals should therefore discuss, with their financial planner or advisor, the merits of each recommendation for their own specific circumstances and realise that not all investments will be appropriate for all subscribers. To the extent permitted by law, Fat Prophets and its employees, agents and authorised representatives exclude all liability for any loss or damage (including indirect, special, or consequential loss or damage) arising from the use of, or reliance on, any information within the report whether or not caused by any negligent act or omission. If the law prohibits the exclusion of such liability, Fat Prophets hereby limits its liability, to the extent permitted by law, to the resupply of the said information or the cost of the said resupply.

Funds Management – In addition to the listed funds FPC, FPP and FATP, Fat Prophets Pty Ltd manages the separately managed accounts, namely Concentrated Australian Shares, Australian Shares Income, Small Midcap, Global Opportunities, Mining & resources, Asian Share, European Share and North American Share. These SMAs are managed under their own mandates by the fund managers, and this is independent to the research reports.

Staff trading – Fat Prophets Pty Ltd, its directors, employees and associates of Fat Prophets may hold interests in many ASX-listed Australian companies which may or may not be mentioned or recommended in the Fat Prophets newsletter. These positions may change at any time, without notice. To manage the conflict between personal dealing and newsletter recommendations the directors, employees, and associates of Fat Prophets Pty Ltd cannot knowingly trade in a stock 48 hours either side of a buy or sell recommendation being made in the Fat Prophets newsletter. Staff trades are pre-approved by an appointed staff trading compliance officer to ensure compliance with the staff trading policy.

For positions that directors and/or associates of the Fat Prophets group of companies currently hold in, please click here.