Wall Street benchmarks extended higher on Tuesday led by technology, and as investors digested Trump’s latest warning on tariffs that would be levelled at not just China, but also neighbouring countries Canada and Mexico. Bonds edged higher, while the US dollar surged to the highest level since mid’23 on the view that tariffs could stoke inflation and slow the pace of Fed rate cuts. Commodities and precious metals stabilised following yesterday’s selloff, while the VIX lost 4% to 14.

The Dow Jones added 0.28%, the S&P 500 gained 0.57% to 6,021 and the Nasdaq Composite advanced 0.63%. The Russell 2000 declined 0.7%. Incoming President Donald Trump said he would impose a 25% conditional tariff on Canadian and Mexican imports that would violate a free-trade deal negotiated during his previous term. Automakers such as Ford and General Motors which have highly integrated supply chains across Mexico and Canada were sharply lower.

Bonds came for sale with yields edging higher with the 10yr adding 4 bps to 4.31%. Trump outlined “an additional 10% tariff, above any additional tariffs” on imports from China, raising the risk of inflation. The Hang Seng and CSI300 were resilient yesterday on the announcement, given the tariffs were lower than threatened by Trump during the election campaign.

After the close, the Fed will release the minutes from the last FOMC meeting, which will be closely parsed for any clues on policy trajectory over the coming year. Tomorrow the Fed’s preferred inflation gauge, the PCE report, will be released which will be influential at the upcoming FOMC meeting in a few weeks’ time.

Trump’s trade and fiscal policies could stoke inflationary pressures and slow down the Fed’s monetary policy easing cycle. Fed official Neel Kashkari, a well-known hawk, said he was open to cutting rates again next month. Markets are still pricing in a roughly 50/50 chance the Fed will go again with another 25 bp cut.

The dollar continued to surge with the DXY adding 0.35% to 107.16. Since the Fed commenced easing with the 50 bp cut in September, the DXY has extended higher by 7%. The dollar index is now hitting up against the top of the channel in place since late ’22 and what could be heavy resistance. Perceived US exceptionalism, Trump’s growth policies and growing risks around inflationary pressures returning next year and delaying further rate cuts have pushed the dollar higher. Equally, the tariffs announced by Trump yesterday have pushed other major currencies lower.

Commodities markets settled from the dollar-induced selloff on Monday with oil stabilising and gold adding back +0.43% to $2653. The sell-off in gold might have been exacerbated by option expiry, which can sometimes be a clearing event if the number of options exercised is high. Silver added 0.64% to $30.50, while platinum was lower by 1%. Copper fell 0.84% to $4.12 while the soft ag complex was predominantly higher.

Morgan Stanley chief strategist Mike Wilson asked the question this week in a note to clients “what’s going to keep valuation levels historically elevated?” referencing the US stock market which is priced at the top end of the range. He concluded that “all told, we think our 12-month forward P/E target of 21.5x (vs. 22x today) reflects the balance of factors and is a reasonable assessment of fair value in an environment of broadening EPS growth and subdued interest rates in our base case”.

Morgan Stanley believes that earnings growth will continue to accelerate next year, which will be supportive of equity markets. “With hard landing risk reduced this fall, the Fed cutting rates, business cycle indicators (which lead EPS growth) showing signs of life and the potential for an animal spirits rebound post the election, the path of earnings growth should be upward as we head through 2025. We expect 13% growth in ’25 in our baseline and 9% in ’24. The combination of these factors should also help to drive a more balanced earnings recovery across sectors and styles, something that has been largely absent.”

Happy days. Mike Wilson was very bearish on the market in 2022 through to the beginning of this year, and then he notably pivoted. While on balance, stock markets should continue to rise next year in a bull market that will turn three years old, international equities in countries such as the UK (and Europe), Japan, Hong Kong/China and Australia should do much better in my view, primarily on valuation grounds.

Bonds have rallied and the dollar has surged on Scott Bessent’s appointment as Treasury Secretary, and expectations that he will reduce the deficit and Federal debt and strive to get fiscal spending down, the reality however might prove to be somewhat more sanguine. This is all easier said than done.

As Morgan Stanley CIO Lisa Shalett noted this week “excluding proposals to extend all 2017 tax cuts, the US deficit is around $2 trillion per year. With mandatory programs accounting for nearly 55% of spending and annual interest payments at $1 trillion, even if all discretionary spending ex defense were eliminated the deficit would still approach $1 trillion just with simple tax cut extension. Meanwhile, competitive currency devaluation could constrain the use of tariffs to incentivize onshoring. In a complex world of policy change, investors should avoid overreliance on generalized macro and passive positioning.”

In other words, “easier said than done.” There is a lot of optimism around a Trump administration being fiscally responsible with some of the key government appointments, but the reality could prove quite different. I doubt for one second that the incoming Trump administration will be successful in reducing the deficit or the Federal debt. For this reason, the precious metals while in correction mode at present, should soon find a floor. I would also expect the US dollar to struggle going much higher above the big resistance level at 107.

With the debt ceiling debate set to come into focus for the markets in January, attention is going to turn to the obvious constraints around debt, deficits and mandatory spending – which cannot be reduced. Lisa Shalett estimates the “US government currently generates approximately $5 trillion in revenue per year to pay for roughly $7 trillion in annual spending obligations. The implication is that with no change to existing policies…the US is slated to run a $2 trillion annual deficit for the next decade, increasing the total debt pile by nearly 65%, to more than $50 trillion.”

Lisa concluded that “it’s easy to make political pronouncements but usually much harder to deliver. This has been especially true with US government spending, most of which is mandatory and covered by acts of Congress, including the more than 50% of spending dedicated to Social Security, Medicare, Medicaid and other programs. Interest payments on US Treasury debt are also non-negotiable.” It is going to be very hard for Trump to get the US deficit and Federal debt down. I agree with Lisa in that this is not about saying there is no waste within government that cannot be reduced, but “the devil is in the details”, and the reality of achieving real impact on debt and deficits likely requires potentially profound choices. I doubt the political will is going to be there until there is some kind of crisis in the bond and currency markets.

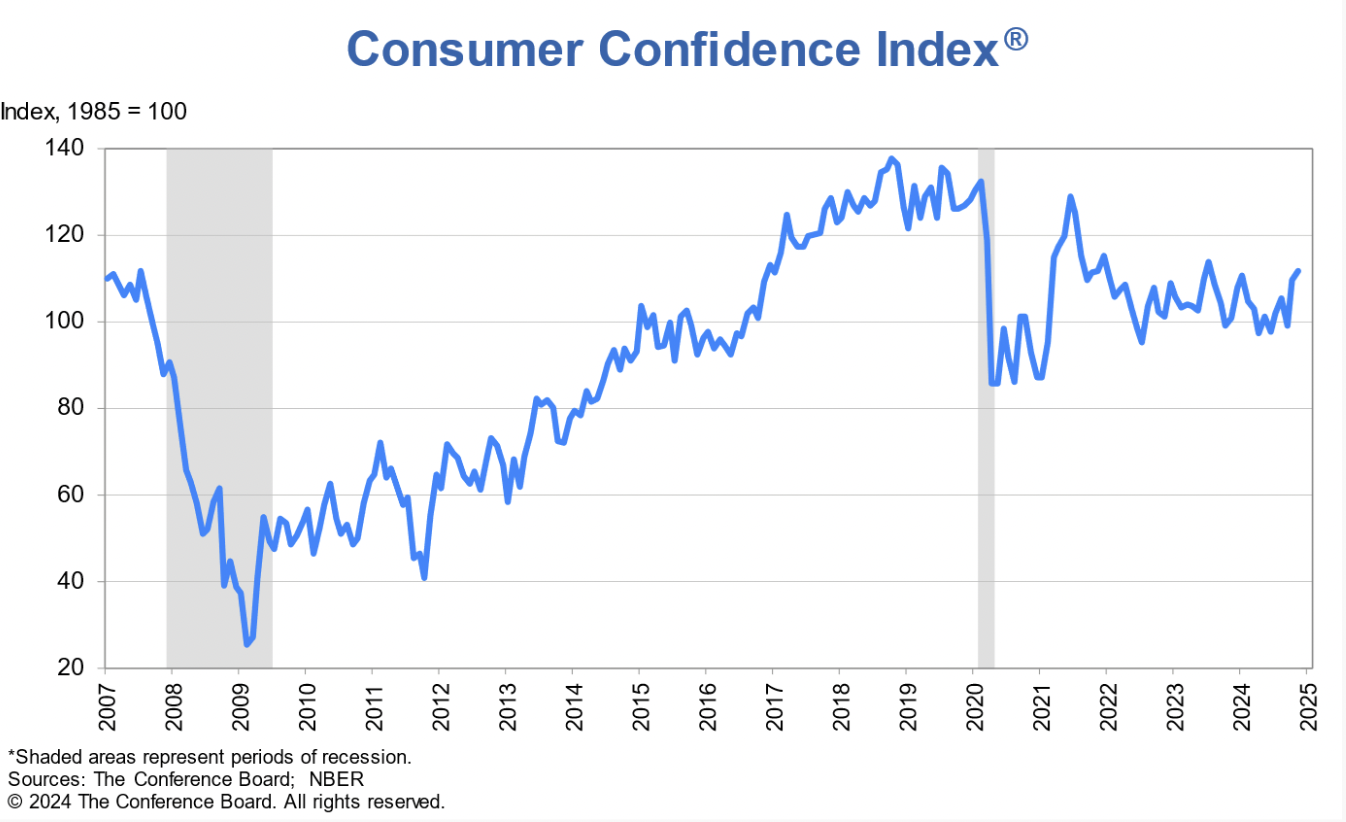

While Trump’s tariff rhetoric dominated investor sentiment, there was also some data to digest. The Conference Board’s Consumer Confidence index strengthened in November, climbing to 111.7 from 109.6 in October. The Present Situation Index, which reflects how consumers view current business and job market conditions, jumped 4.8% points to 140.9. Meanwhile, the Expectations Index, which gauges short-term outlooks for income, business, and jobs, saw a modest increase to 92.3. The index suggests consumer confidence at the top of the range we have seen over the past couple of years.

November’s increase was mainly driven by more positive consumer assessments of the present situation, particularly regarding the labour market. Compared to October, consumers were also substantially more optimistic about future job availability, which reached its highest level in almost three years. Meanwhile, consumers’ expectations about future business conditions were unchanged and they were slightly less positive about future income.”

The ASX200 retreated -0.69% to 8,485 on Tuesday, dragged down by tumbling energy stocks, banks and some miners. Weighing on investor sentiment was tariff rhetoric from US President-elect Donald Trump, stoking fears of global trade disruptions. The Australian dollar fell sharply below 65c when the news hit the wire. While there were no major local economic releases, the monthly CPI indicator is on the agenda this morning and will be closely parsed. SPI futures are pointing to a 0.48% gain on the open.

Since breaking up through the major resistance level at 7,500, the ASX200 has extended higher by 1000 points to reach nearly 8,500. The index has hit the top of the channel which raises the scope for a near-term pullback, however, the big-picture technical setup on the 20-year chart below, favours an upside extension next year towards our bull market target of 9,000. The well-defined trend channel that has been in place for fifteen years continues to demonstrate remarkable consistency.

Yesterday investors’ nerves were somewhat frayed by Trump’s announcement of plans to impose fresh 25% tariffs on goods from Mexico and Canada while adding another 10% tariff on Chinese goods (well below previous threats in China’s case) from day one of his presidency.

Turning to Asia, China’s CSI 300 dipped -0.21% and the Hang Seng +0.04% was flattish at the close after giving up earlier gains. There was a sense of relief after Trump stated he would impose a further 10% tariff on Chinese goods, well below earlier threats of 60% and the 40% economists anticipated. Greater China stocks had already re-rated lower on those threats. Of course, there remains some lingering uncertainty about the mercurial Trump and whether that figure could change when he assumes office in January.

In Japan, benchmarks fell on fears that Trump’s proposed tariffs on China, Canada and Mexico could eventually expand to Japan. The Nikkei slid -0.87% to 38,442, while the broader Topix dropped -0.96%. Losses were led by exporters, energy and banking stocks. The yen was relatively little changed, settling around the 154 range in late afternoon trading. The 10-year JGB yield dipped 1bps to 1.06%.

London’s stock markets ended in the red on Tuesday as risk aversion intensified following Donald Trump’s proposal for new tariffs targeting Canada, Mexico, and China, which reignited concerns about global trade tensions. The FTSE 100 dropped -0.4%, closing at 8,258 points, while the mid-cap FTSE 250 saw a sharper decline of -0.87%.

On the continent, in the absence of major regional economic news, European bourses faced widespread losses as concerns over potential US trade tariffs weighed heavily on sentiment. While the proposed tariffs currently target North American countries and China, the possibility of future measures against European manufacturers, especially in the auto sector, unnerved investors. Shares of carmakers such as Stellantis, Volkswagen, and BMW declined, as did auto suppliers.

At the close, the pan-European Stoxx 50 was down -0.79%, Germany’s DAX subtracted -0.56%, while France’s CAC-40 declined -0.87%. Italy’s FTSE MIB retreated -0.78%, while Spain’s IBEX 35 fell -0.80%.

Carpe Diem!

Angus

Disclosure: Fat Prophets and its affiliates, officers, directors, and employees may hold an interest in the securities or other financial products relating to any company or issuer discussed in this report. Fat Prophet’s disclosure of interest related to Investment Recommendations can be provided upon request to members@fatprophets.com.au.

Chart Source: Thomson Reuters