EVN

EVN Snapshot

Good Leverage

Evolution Mining (Evolution) released its December 2022 quarter operational results, and in doing so has revealed a good performance. Evolution levered into a higher gold price by lifting gold production and reining in unit operating costs. Guidance for 2023 was maintained. Mine cashflows for the quarter were well supported by a higher realised gold price and better operational performance. A snapshot of the balance sheet shows the structure remains very sound as of 31 December 2022.

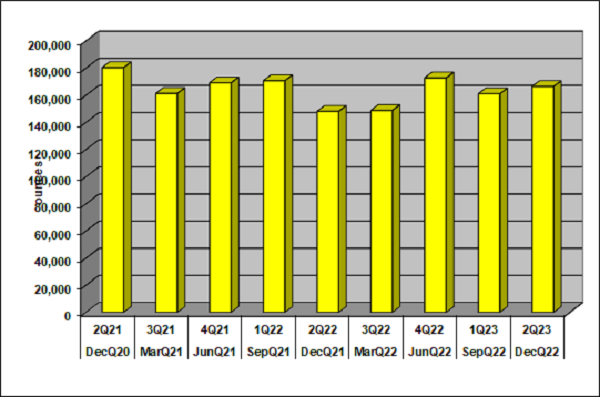

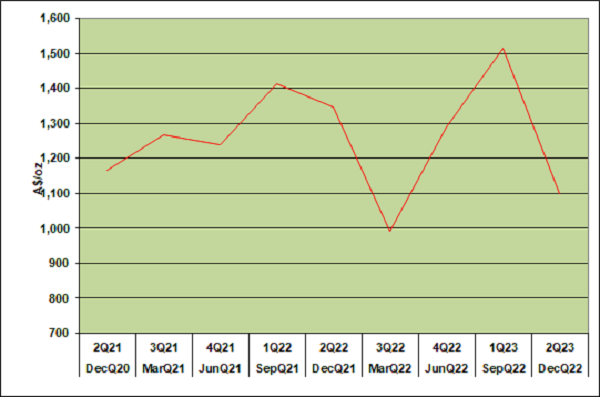

Gold production for the December 2022 quarter came in higher, with the following chart showing quarterly gold production:

Source: Evolution

For the December 2022 quarter, Evolution reported a 12.4% year-on-year (yoy) rise in gold production, to 166,404 ounces, with four of Evolutions’ five mines in Cowal, Mungari, Ernest Henry and Red Lake contributing higher production outcomes. Mt Rawdon was the only mine in negative territory. The December 2022 quarter was, in our view a good one, especially as Evolution was able to lever into a higher gold price environment coupled with a fall in unit costs.

Gold production for 2023 is forecast to be 720,000 ounces ± 5.0%. In 2022, Evolution produced 640,275 ounces of gold, with the forecast production pick up now a very pleasing aspect of Evolutions future value creation potential.

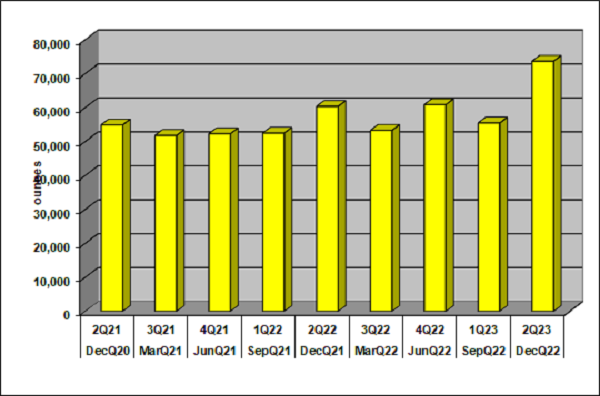

Evolution’s biggest producer in Cowal was the standout, turning in a solid 22.0% yoy increase in gold production for the quarter, to 73,676 ounces. The following chart shows quarterly gold production for the Cowal mine:

Source: Evolution

Driving the result was a rise in milling of ore throughput of 86% yoy, to 4.4 million tonnes for the quarter, with mine scheduling a key factor. A partial drag were gold grades and gold recoveries recording falls. Gold grades fell to 0.96 of a gram per tonne gold from 0.97 of a gram per tonne gold from a year earlier, while gold recoveries fell to 83.9% from 84.2% for the comparative year. This was, in our view, a very solid result by Cowal.

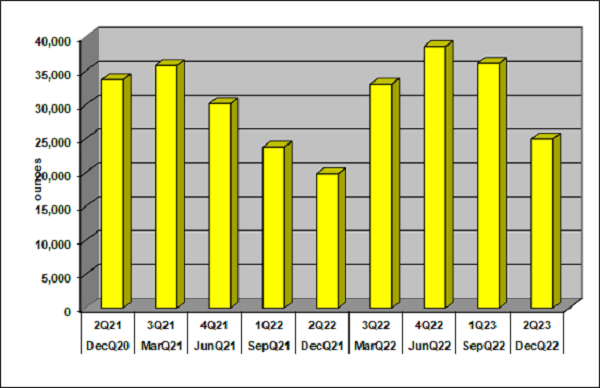

Red Lake was also a standout for the quarter, given the mine has had a chequered past. The following chart shows quarterly gold production:

[subscribe_to_unlock_form]

Source: Evolution

Red Lake reported a 25.9% increase in gold production yoy for the December quarter, to 24,960 ounces. The mine reported improvements for ore throughput in the mill, gold grades and gold recoveries for the reported quarter.

Mungari reported a 1.7% yoy increase in production to, 35,011 ounces of gold for the reported quarter. Dragging on the overall result were Mt Rawdon and Ernest Henry following the reporting of falls yoy of 5.2% and 11.1% respectively, to 11,003 ounces of gold and 2200 ounces. Mt Rawdon experienced above average rainfall and Ernst Henry production was impacted by planned infrastructure shut ins.

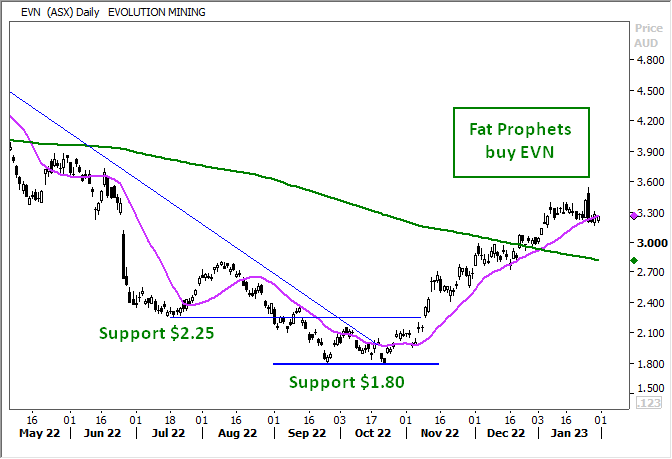

The daily chart for EVN indicates the price has remained above the 20 period simple moving average and is currently consolidating around the $3.30 level, this level is also the consolidation range shown in May – June 2022

Evolution produces silver and copper as by-products, with both reporting better production outcomes for the quarter. Silver production jumped 51% yoy, to 142,055 ounces and copper by 275% yoy, 15,483 tonnes.

Unit operating costs were a standout for the quarter, with the reporting of an improvement. For the December 2022 quarter, all-in sustaining costs (AISC) fell 18.4% yoy, to A$1,099 an ounce. The following chart shows quarterly AISC:

Source: Evolution

Driving the better result was higher by-product credits for silver and copper. Higher mining and processing activities were a partial offset from higher by-product credits. Mining costs jumped 32.5% yoy, to A$1,024 an ounce and processing costs jumped 26.6% yoy, to A$570 an ounce. Costs were impacted by a lack of labour and equipment.

AISC guidance for 2023 is expected to fall around A$1,240 ± 5.0% an ounce and was unchanged. Evolution beating this number will be an excellent result, given the persistent inflationary pressures in the industry.

Evolution reported a rise of 7.3% yoy in its average realised gold price for the reported quarter, to A$2,551 an ounce. Evolution will generate robust cash flows and operating margins, given the Australian dollar gold price of A$2,707 an ounce. Evolution will report its interim 2023 financial results in February 2023, and we expect a satisfactory result but rising costs will be a feature.

We hold a positive view on the gold price and expect it to retest 2023 highs, on the current US$1,924 an ounce. Persistently high inflation and a weaker US Dollar will provide the tailwinds over the course of 2023.

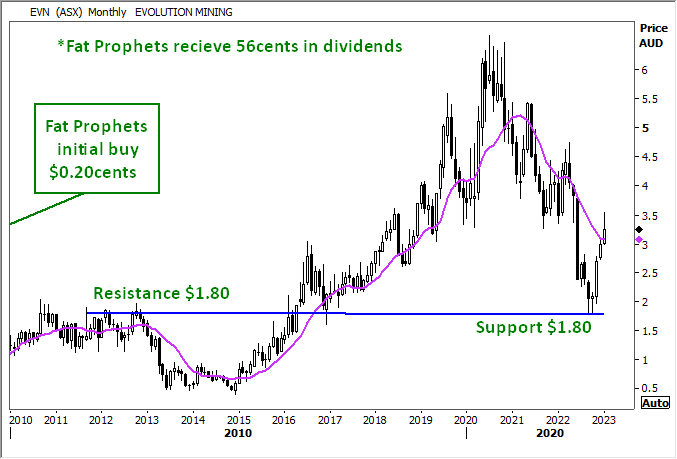

The monthly chart of EVN highlights the rapid rise above the $1.80 support level, current price movements are above the 12 month moving average, however current movements also remain within the down channel

Moving on, and for the December 2022 quarter, net mine cash flow rose 8.9% yoy, to A$75.5 million. Greater mining activities, higher costs and a jump in capital spending were headwinds on operating cash flow for the quarter.

As of 31 December 2022, cash stood at A$313.2 million, compared to A$422.2 million from a year earlier. We are comfortable with the cash position.

Operationally, the December 2022 quarter numbers were good, with Evolution levering into higher gold prices. There were certainly gems hidden in the result, such as the Red Lake outcome and the improvement in unit costs. We hold to the belief that Evolution remains well positioned to lever into our scenario of a higher gold price going forward, following a period of reshaping its portfolio. Coming from a sound financial position and a management team we believe can add long-term value warrants support for the stock.

Consequently, we continue to recommend Evolution Mining as a buy for Members with no exposure to the stock.

Disclosure: Interests associated with Fat Prophets holds shares in Evolution Mining.

[/subscribe_to_unlock_form]Fat Prophets has made every effort to ensure the reliability of the views and recommendations expressed in the reports published on its websites. Fat Prophets research is based upon information known to us or which was obtained from sources which we believed to be reliable and accurate at time of publication. However, like the markets, we are not perfect. This report is prepared for general information only, and as such, the specific needs, investment objectives or financial situation of any particular user have not been taken into consideration. Individuals should therefore discuss, with their financial planner or advisor, the merits of each recommendation for their own specific circumstances and realise that not all investments will be appropriate for all subscribers. To the extent permitted by law, Fat Prophets and its employees, agents and authorised representatives exclude all liability for any loss or damage (including indirect, special, or consequential loss or damage) arising from the use of, or reliance on, any information within the report whether or not caused by any negligent act or omission. If the law prohibits the exclusion of such liability, Fat Prophets hereby limits its liability, to the extent permitted by law, to the resupply of the said information or the cost of the said resupply.

Funds Management – In addition to the listed funds FPC, FPP and FATP, Fat Prophets Pty Ltd manages the separately managed accounts, namely Concentrated Australian Shares, Australian Shares Income, Small Midcap, Global Opportunities, Mining & resources, Asian Share, European Share and North American Share. These SMAs are managed under their own mandates by the fund managers, and this is independent to the research reports.

Staff trading – Fat Prophets Pty Ltd, its directors, employees and associates of Fat Prophets may hold interests in many ASX-listed Australian companies which may or may not be mentioned or recommended in the Fat Prophets newsletter. These positions may change at any time, without notice. To manage the conflict between personal dealing and newsletter recommendations the directors, employees, and associates of Fat Prophets Pty Ltd cannot knowingly trade in a stock 48 hours either side of a buy or sell recommendation being made in the Fat Prophets newsletter. Staff trades are pre-approved by an appointed staff trading compliance officer to ensure compliance with the staff trading policy.

For positions that directors and/or associates of the Fat Prophets group of companies currently hold in, please click here.