Rio Tinto (ASX: RIO)

![]()

Rio Tinto (Rio) has just reported its third quarter operational results to 30 September 2022, revealing generally firmer production results across many of its product offerings. The operational result meant 2022 guidance remained unchanged, except for copper, while iron ore was guided toward the lower end of the range. The following table shows a summary, by product offering, of Rio’s operational results for the September quarter 2022:

Source: Rio Tinto

Overall, we rate Rio’s September quarter operational performance as good, given the market environment in which it was generated. On the commodity prices front, these were weaker over the quarter and will have a negative impact, leading to a lower full year 2022 financial result. Operations should, with the current momentum, at this stage, have a positive impact. Supporting our rating and providing some comfort in the September quarter result, was Rio maintaining 2022 guidance for all its product offerings except for copper.

To the operational positives first and one was, Rio’s key iron ore offering and as Members saw from the above table, iron ore delivered a positive outcome for the quarter. The following chart shows quarterly iron ore production:

Source: Rio

Iron ore production rose by 2.3% year-on-year (yoy), to 73.7 million tonnes. Rio’s key Pilbara operations reported a 1.8% yoy increase, to 71 million tonnes. Driving this result were the commissioning of the Gudai-Darri site and the Robe River (Rio’s interest 53%) ramping up. The Pilbara’s six Hamersley sites delivered a 1.8% yoy increase, to 56.7 million tonnes. In passing, Gudai-Darri will deliver 43 million tonnes of iron ore per annum over a 40 year mine life. Full capacity will be reached in 2023, while product quality mix will continue to improve as ramp up continues. Gudai-Darri is Rio’s most advanced and automated operation. Iron Ore Company of Canada (IOC) reported a 28.3% yoy increase in production, to 2.8 million tonnes of concentrate and pellets.

The daily view of RIO indicates the price remains within a large trading range with support indicated at $87.60 and resistance shown at $100.00. Following the down trend movement from the March 2022 highs, this current basing pattern can be the precursor to resuming the underlying trend[subscribe_to_unlock_form]

Production guidance for iron ore in 2022 (100% basis), was unchanged with a forecast in the range of 320 million tonnes to 335 million tonnes. Rio did however guide toward the lower end of the range. IOC is forecast to produce concentrate and pellets in the range of ten million tonnes to 11.0 million tonnes in 2023 and was unchanged. In 2022, Rio produced 321.6 million tonnes (100% basis) of iron ore in 2021

Pleasingly and a feature, was iron ore unit cost guidance for 2022, remained unchanged in the range of US$19.50 per tonne to US$21.00 per tonne and was unchanged. With iron ore trading around US$95 per tonne, at the time of writing, operating cash flows and margins will remain substantial.

Copper, both mined and refined turned in good performances for the quarter, with mined copper the standout. The following chart shows quarterly mined copper production:

Source: Rio

Mined copper reported a 10.2% rise yoy, to 138,000 tonnes. Behind the result was Rio’s Escondida mine (Rio’s interest 30%), following a 9.8% rise, yoy, in mined copper production, to 75,100 tonnes. Driving this result was the mining of high copper graded ore. Kennecott added to the better performance for the quarter, following the reporting of a 19% rise in production yoy, to 50,700 tonnes, on higher copper grades as well.

Guidance for mined copper production in 2022 was unchanged and is forecast in the range of 500,000 tonnes to 575,000 tonnes. For 2021, Rio produced 494,000 tonnes of mined copper, with the forecast uplift in production a pleasing feature, and will partially offset the impact of weaker copper prices on the 2022 financials.

Rio does not report actual unit costings for copper but did provide an update on 2022 guidance. Copper C1 unit cost (applicable to both refined and mined copper) guidance for 2022 was downgraded to a forecast in the range of US$1.50 per pound to US$1.75 per pound from the previous US$1.30 per pound to US$1.50 per pound, citing inflationary pressures and operating equipment and labour shortages. Although the downgrade is a disappointment, with copper prices trading around US$3.51 per pound, operating cash flows and margins will remain substantial.

The September 2022 quarter for refined copper was a good one, with production ahead by 7.1% yoy, to 54,100 tonnes. he following chart shows quarterly refined copper production:

Source: Rio

Delivering the better performance was the Kennecott operation, with the reporting of a 9.8% rise in refined copper production yoy, to 39,200 tonnes. Driving this result was the milling of higher grade ore.

Despite the strong September quarter performance, Rio downgraded its 2022 guidance for refined copper production to be in the range of 190,000 tonnes to 220,000 tonnes, from the previous 230,000 tonnes to 290,000 tonnes. Rio cited the reliability of Kennecott with a major rebuild due in 2023 as the reason for the revision. The downwardly revised guidance range remains around the 201,900 tonnes of refined copper delivered in 2021.

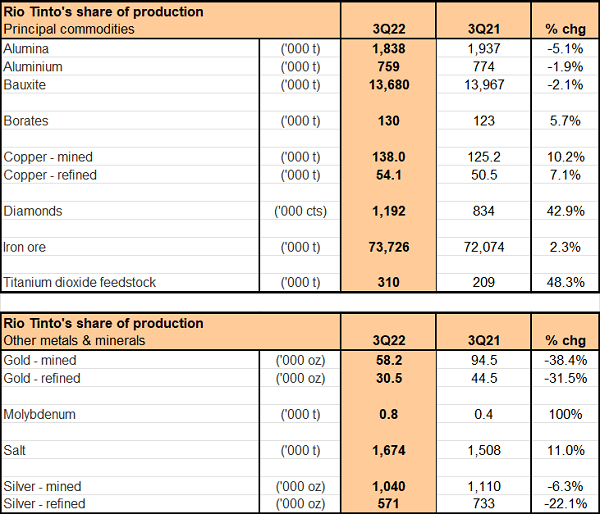

Diamonds reported a better performance for the September quarter, following the printing of a 42.9 yoy rise, to 1.2 million carats. The following chart shows quarterly diamond production (Rio’s Argyle mine reached its end of life in the December quarter 2020):

Source: Rio

The Diavik mine is Rio’s sole diamond operation and reported a surge of 42.9% yoy, to 1.2 million carats. Rio lifted its interest in the Diavik mine from 60% to 100% from November 2021.

Diamond production guidance for 2022 was pleasingly left unchanged and is forecast to be in the range of 4.5 million to 5.0 million carats. In 2021, Rio produced 3.8 million carats, with the uplift in 2022 due to the interest change in Diavik.

A real feature of the September quarter result, albeit both are minor product offerings, was the performance of molybdenum (moly) and salt. Moly reported a 100% yoy surge, to 8,000 tonnes, while salt production was 11.0% higher yoy, to 1.7 million tonnes. Rio does not provide published guidance numbers for its minor product offerings.

Rio’s aluminium operations turned in a softer performance for the September quarter, with all three product offerings reporting falls in production.

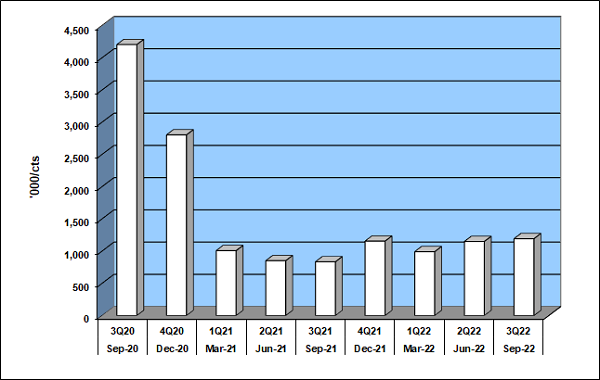

Bauxite production fell 2.1% yoy, to 13.7 million tonnes. Rio reported lower production out of Weipa and Gove. The following chart show quarterly production for bauxite:

Source: Rio

Rio’s biggest producer in Weipa was a key contributor, with the reporting of a 4.3% fall in production yoy, to 8.4 million tonnes. Contributing as well was Gove, following the reporting of a 5.3% fall yoy, to 2.9 million tonnes. Lower operational efficiencies and infrastructure availability across all the company’s sites, drove their overall lower result.

Production guidance for 2022 for bauxite was unchanged with a forecast in the range of 54 million to 57 million tonnes. In 2021, Rio delivered 54 million tonnes of bauxite.

Alumina production for the September quarter fell by 5.1% yoy, to 1.8 million tonnes. The following chart show quarterly production for alumina:

Source: Rio

Queensland Alumina (Rio’s interest 80%) and Yarum were key contributors, reporting yoy falls of 10.3% and 7.1% respectively, to 662,000 tonnes and 715,000 tonnes. Both sites were impacted by lower infrastructure efficiencies. A partial offset was São Luis (Rio’s interest 10%), following the reporting of a 26.7% rise yoy, to 95,000 tonnes. São Luis continue to ramp up after restarting in November 2021.

Alumina guidance for 2022 was left unchanged and is forecast to be in the range of 7.6 million to 7.8 million tonnes. In 2021, Rio produced 7.9 million tonnes of alumina.

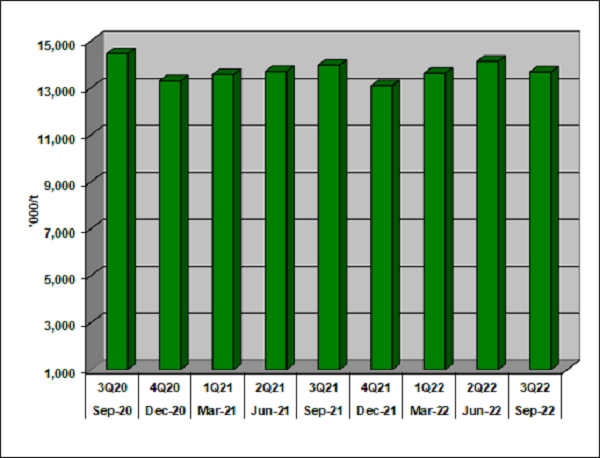

Downstream aluminium finished the trio of poor results for the quarter, following a 1.9% fall yoy, to 759,000 tonnes. The following chart shows quarterly aluminium production:

Source: Rio

Behind the lower result was Rio’s three Australian operations, delivering a 5.9% fall yoy, to 304,000 tonnes. Operational issues including labour and equipment availability were drivers of the lower September quarter outcome. Rio’s Canadian refineries reported a flat number, falling just 0.2% yoy, to 616,000 tonnes.

Production guidance for aluminium in 2022 left unchanged and is forecast to be in the range of 3.0 million to 3.1 million tonnes. In 2021, Rio produced 3.2 million tonnes of aluminium.

Exploration and evaluation expenditure charged to the profit and loss account for the September 2022 quarter came in at US$226 million, compared to US$192 million for a year earlier, representing a 17.7% yoy rise. Copper exploration consumed circa 39% of the spend for the quarter: central 31%, minerals 22% and 8% to iron ore. We are pleased with the modest uptick, as Rio has sufficient brownfield opportunities that are less capital intensive to explore.

The monthly view of RIO highlights the long-term support level at $86.00. Currently, the primary trend remains up as the price consolidates above support and moves below the 12 month moving average

Given the trading environment and especially the tightening rate cycle, we consider Rio delivered a good September quarter result. We take comfort most of Rio’s guidance numbers for 2022 remaining unchanged. We have a positive outlook for iron ore and base metals in the latter part of 2023 and into 2024. A weaker US Dollar should prove to be a tailwind for commodity prices in 2024 especially, as the US debt pool grows because of stimulatory initiatives and the US economy shrinks in value. We consider Rio remains leveraged to a weaker US Dollar thematic.

Rio’s headline 2022 financial numbers will be lower than its 2021 full year result, but due to Rio’s cost advantages across many of its product offerings, cash flows and profits will remain robust. The 2022 dividend will also fall on lower cash flows, but the current correction in the share price does, in our view, undervalue Rio.

Consequently, we continue to recommend Rio Tinto as a buy for Members without exposure.

Disclosure: Interests associated with Fat Prophets holds shares in Rio Tinto.[/subscribe_to_unlock_form]